What is the Real Cost to Africa Not Using the PAPSS?

April 28, 2026

Impact of Taxes on Women Entrepreneurs in Cameroon

April 29, 2026

Introduction

Cameroon signed the African Continental Free Trade Area (AfCFTA) in 2018 with 43 other African countries designed to accelerate intra-African trade and enhance economic integration by reducing trade barriers and harmonizing policies across the continent. It will boost Africa’s position across global markets and strengthen its common voice. The AfCFTA could boost African incomes by by $450 billion, while Kouam et al (2024) find that Cameroon’s GDP could be 2.5% higher by 2030 if the AfCFTA is properly implemented.

The AfCFTA is an opportunity for Cameroon to pursue market-oriented reforms to accelerate inclusive economic development. Since 2018, a number of reforms were enacted to support free enterprise in Cameroon, from zero-tariff inputs in agriculture and the energy sector, digitizing some public services and harmonizing the ECCAS customs code. This policy brief provides an overview of reforms that support economic freedom and illustrate how they align with the AfCFTA. Far from being self-congratulatory, it seeks to provide a framework to accelerate market-friendly reforms to boost entrepreneurship and economic freedom in Cameroon.

Section 1: How the AfCFTA Prompted Free Market Reforms in Cameroon

Since signing the AfCFTA in 2018 and ratifying it in 2019, policymaker shave been intentional about implementing the AfCFTA. Cameroon published its e-tariffs book and began trading under the Guided Trade Initiative (GTI). Lower tariffs come with risks for businesses, despite its ability to lower prices for consumers through competition. To support businesses in the energy, water and agriculture sector, policymakers suspended import duties for vital inputs like solar panels, electric vehicles, fertilizer and farm equipment to support local entrepreneurs. For local producers of flour (Art. 142, 16-b)and eggs, policymakers reduced value added tax (VAT) in the 2024 budget and reduced them to zero in 2025 following CEPI’s advocacy.

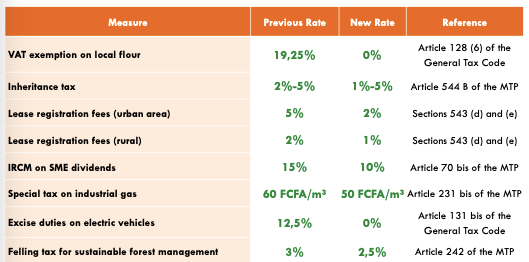

In 2018, policymakers removed export taxes for industrial products, animal and vegetal products that have been transformed in Cameroon. In 2025, businesses saw a reduction of registration duties on residential leases from 5% to 2% in urban areas and 2 to 1% in rural areas (Art. 543, d and e). Large companies equally benefitted from easier conditions for tax audits, reducing paper work and compliance cost for large businesses. The deductibility of bad debt was simplified and the automatic deduction threshold was reduced from 500,000 to 3 million. The table below provides a summary of more reforms that reduce the cost of operation of businesses.

Summary of Tax relief in 2025

In 2026, businesses who hire employees below 35 for their first jobs are not required to pay income taxes but must pay social security contributions. At face value, such reforms are ideal only for businesses who comply and can afford accountants to follow-up deductions and rebates.

Section 2: The AfCFTA has Prompted Market Friendly Reforms

Reforms designed to promote free trade have grown since 2018, when compared to the 2012 – 2017 period where much of the support was through subsidies that were not accessible to the majority of businesses. For Mme. Ndah Mirabel (Director of Internal Trade), reforms designed to boost local entrepreneurship are vital as they allow businesses time to prepare for. Amore competitive post-AfCFTA trading period. Policymakers are accelerating efforts to promote local products through the import substitution and range of incentives as they implement the AfCFTA. This is important as CEPI’s agro-industrial sector will face intense competition from more industrialized peers across Africa. The current reforms designed to promote formal entrepreneurship and free enterprise will reduce cost for most formal businesses, allow newer firms to employ mor people and for artisanal producers who make up 99% of the economic fabric to sell their products to formal businesses.

Cameroon’s decision to join the AfCFTA creates a market of 1.4 billion people but it equally opens up Cameroon’s market to more competition from abroad. These reforms will boost entrepreneurship but policymakers must be more intentional about accelerating the industrialization by ensuring that the subsidies are linked to measurable targets

Section 3: The role of Free Trade in Driving Free market Reforms in Cameroon

The African Continental Free Trade Area (AfCFTA) is a pillar of the free markets in Cameroon. The AfCFTA extends the principles of competition, voluntary exchange and efficient resource allocation beyond Cameron’s borders, allowing the invisible hand to operate regionally. Meanwhile, the free markets operate within countries and in the case of Cameroon removes government-imposed barriers (tariffs, quotas, regulations) that slow or prevent international exchange and foster a more competitive and efficient global economy.

The AfCFTA is driving free market reforms in two ways; firstly, it is causing policymakers to accelerate reforms that promote local industry and boost exports. It is however, to note that some reforms that include subsidies can be disruptive, but limited tax holidays and technical support for exporters will generate positive returns over the long run.

However, the focus in on boosting internal trade capacity as Cameroon still underproduces a lot of the food it needs. Fiscal incentives in the budget are designed to boost the attainment of the import substitution strategy while lower import duties for vital inputs are designed to promote local manufacturing. However, progress is slow as manufacturing as a percentage of GDP is estimated at 14% versus 18% in 2018.

However, the economy as a whole has grown even as we expect manufacturing to play a more important role in GDP growth. If one looks at the Frasier Institute’s freedom index, Cameroon has declined over the years, showing that the AfCFTA may have not advanced economic freedom, despite the improvement in aspects of free enterprise.

Proposed Solutions & Pathways to Accelerate Free Enterprise

- While tax holidays for hiring youth are commendable, they only benefit the small formal sector. To truly capture the forecasted 2.5% GDP boost from AfCFTA, Cameroon must replace complex tax compliance with a unified low-cost approach that automates registration and social security, bypassing expensive accountants. This will encourage more informal production units to formalize their activities.

- Manufacturing as a share of GDP has dropped from 18% to 14% despite subsidies. It is essential for policymakers to shift from picking winners through fiscal incentives to strengthening property rights, the legal system and make it easier to do business. This includes, but is not limited to, digitizing land titles and creating specialized fast-track commercial courts for AfCFTA-related disputes that are reliable and transparent.

- Optimize the Energy-Trade Nexus Since import duties on solar panels and fertilizers have persist, the next step is liberalizing the energy distribution market. For example, allowing private micro-grids to sell power to agro-industrial hubs will lower the “cost of operation” much more that tax rebates.

- While e-tariff books are useful, the primary “tax” on Cameroonian entrepreneurs is the time lost at roadblocks and bureaucratic bottlenecks. Policymakers should harmonize the ECCAS customs code and make sure that the made in Cameroon goods can move freely as intended across the sub-region.

Conclusion

While the AfCFTA has prompted policymakers to enact specific reforms, the decline in the Fraiser Institute’s freedom index highlights a disconnect between high-level trade policy and institutional reality. To unlock the projected 2.5% GDP growth, policymakers must move beyond “picking winners” with subsidies and prioritize systemic legal reforms. If we strengthen property rights and simplify the regulatory burden for artisanal producers, Cameroon will be able to transform the AfCFTA from a competitive threat into a sustainable engine for inclusive sustainable development.

Reference List

- Cameroun, Loi n°2024/013 du 23 décembre 2024 portant loi de finances de la République du Cameroun pour l’exercice 2025, disponible sur le site de la Direction Générale des Impôts : https://impots.cm/

- Direction Générale du Budget. (2018). Cameroun – Loi de finance 2018. Ministère des Finances du Cameroun. https://www.dgb.cm/news/cameroun-loi-de-finance-2018/

- Henri, Kouam. “A Review of Cameroon’s Implementation of the African Continental Free Trade Area (AfCFTA).” J Glob Entrep Manage (2025): 132 . DOI: 10.59462/3068-174X.3.3.132

- Kouam, H., Nchofoung, T., Djamo, H., Tchoffo, R. (2024). The impact of the Economic Partnership Agreement and the African Continental Free Trade Area, Cameroon Economic Policy Institute (CEPI), Henri Kouam Foundation. https://camepi.org/wp-content/uploads/2024/10/The-Impact-of-the-Economic-Partnership-Agreement-and-the-African-Continental-Free-Trade-Area-2-1.pdf

- Kouam, Henri, Tariffs and Trade: Unpacking the Economic Ripple Effects of Trump Tariffs on Africa (September 01, 2025). Available at SSRN: https://ssrn.com/abstract=5988174 or http://dx.doi.org/10.2139/ssrn.5988174

- World Bank. (2020, July 27). Trade pact could boost Africa’s income by $450 billion, study finds. https://www.worldbank.org/en/news/press-release/2020/07/27/african-continental-free-trade-area.

- World Bank. (2025). Manufacturing, value added (% of GDP) – Cameroon. World Development Indicators. https://data.worldbank.org/indicator/NV.IND.MANF.ZS

Authors

Henri Kouam, Executive Director

Dr. Annie Nkeng, Research Fellow

Seraphin Mbarga, Research Analyst

{kind=link}