Reducing Post-Harvest Food Loss in Cassava and Tomato Value Chains in Cameroon

April 25, 2026

Artificial Intelligence & Economic Freedom in Cameroon

April 25, 2026

Executive Summary

Small and Medium-sized Enterprises (SMEs) constitute the backbone of African economies. Even though they are usually very small (e.g., 59% of them in Cameroon), SMEs contribute over 60% of employment and 40% of GDP. However, Africa’s financing gap for SMEs is estimated at $300 billion, severely constraining their working capital and investment, and ultimately impacting overall economic growth and job creation in the region. Traditional financial institutions often fail to support SMEs due to information asymmetries, high transaction costs, stringent collateral requirements, and inadequate risk assessment models. Fintech innovations, including alternative credit scoring, crowdfunding platforms, and mobile money systems, directly address these barriers by reducing operational costs, enabling cash-flow-based lending, and leveraging digital footprints for creditworthiness assessment. Policymakers must adopt a regulatory sandbox approach to foster fintech innovation while ensuring robust consumer protection and data security frameworks.

Key Words: Financial Inclusion, Banking, Credit, Credit Scoring, SMEs

The SME Financing Gap

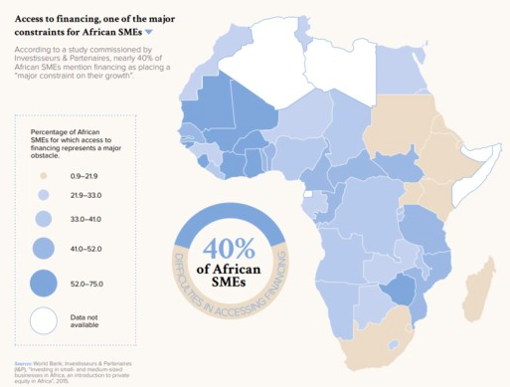

60 million formal SMEs in Africa have an unmet financing need of $300 billion every year (Fedder, 2024). In Sub-Saharan Africa (SSA), this challenge is particularly acute, with 40% of SMEs identifying the lack of access to finance as the primary factor constraining their growth (Figure 1).

Figure 1. Lack of access to finance is constraining SMEs’ growth in Africa. Source: Fedder (2024).

This financing gap represents more than a statistical challenge. Indeed, it embodies unrealized potential for millions of entrepreneurs whose innovative ideas and business ventures could drive economic transformation across the continent. The disparity between capital demand from SMEs and supply from traditional financial institutions has created a systemic barrier to inclusive economic growth.

This brief examines the structural barriers that prevent SMEs from accessing finance and demonstrates how fintech solutions are uniquely positioned to bridge this gap. It concludes with actionable policy recommendations designed to harness fintech’s transformative potential while mitigating associated risks.

Why Traditional Finance Fails to Support SMEs?

Traditional financial institutions (banks, microfinance, etc.) struggle to serve SMEs effectively due to several interconnected challenges:

Information Asymmetry: SMEs often lack the comprehensive credit histories and formal financial records required by traditional banks. Indeed, individuals running SMEs in SSA often lack a formal account, for many reasons, such as income insufficiency, high cost of opening and maintaining an account, remoteness of branches, documentary requirements, and lack of trust (Klapper et al., 2019). In addition, many operate in the informal economy without standardized accounting practices or audited financial statements, making risk assessment difficult and expensive for conventional lenders.

High Transaction Costs: The costs of processing, underwriting, and monitoring small loans often exceed their profitability under traditional banking models. Indeed, banks face similar administrative costs whether processing a $1,000 or $100,000 loan, making smaller SME loans economically unviable. In Cameroon, firm size and location significantly affect access to formal financing, suggesting that smaller firms are disproportionately excluded due to fixed costs and risk perceptions (Kenmegni, 2022).

Collateral Requirements: Traditional banks typically require tangible assets (e.g., land, machinery, and homes) as loan security; however, many SMEs, especially women-led SMEs, lack acceptable collateral, such as real estate or established inventory (Kouam & Kouam, 2024). This asset-based lending approach excludes promising businesses with strong cash flows but limited physical assets.

The Fintech Solution: Overcoming Specific Barriers

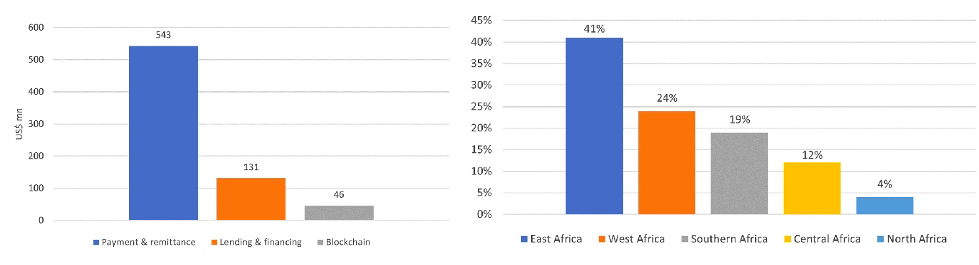

Figure 2. Investment in fintech (a) and fintech-based financing (b) in Africa. Source: (Rafiq, 2021)

Geographic and Infrastructure Constraints: Many SMEs operate in rural or underserved urban areas with limited bank branch networks, creating physical barriers to accessing financial services and relationship-building opportunities with lending officers.

Inadequate Risk Assessment Models: Conventional credit scoring models rely on historical financial data and established credit relationships. In countries like Cameroon with low financial inclusion, these models poorly serve agile, rapidly evolving small businesses whose financial profiles may not conform to traditional banking parameters (Kouam & Kamdem, 2025).

Across Africa, fintechs are more active in payment and remittances compared with the lending and financing segments of the market (Figure 2.a). However, fintech-based financing already constitutes a significant part of total financing on the continent, particularly in East Africa (Figure 2.b). Indeed, fintech innovations, often in partnership with traditional financial institutions, directly address the barriers that traditional finance faces when serving SMEs:

Digital Payment Integration and Alternative Data for Credit Assessment: Fintech platforms leverage non-traditional data sources, including mobile money, phone and internet usage patterns, utility payment histories, social media activity, and e-commerce transaction records to assess creditworthiness (Benlamine & Tressel, 2021; Björkegren & Grissen, 2018). This approach enables lenders to evaluate SMEs that lack conventional credit histories, while providing more nuanced risk profiles. Fintech lending is already well developed in East Africa, with digital platforms such as M-Shwari in Kenya. Central and West Africa are still lagging. Nonetheless, fintech micro-lending services such as MoMoKash, launched in Côte d’Ivoire and Cameroon in 2018 and 2023 by MTN Mobile Money, are beginning to emerge, providing promising prospects.

Automated Underwriting and Reduced Costs: Artificial intelligence and machine learning algorithms automate loan application processing, underwriting, and disbursement, dramatically reducing operational costs and exclusion (Tantri, 2021). Wonga in South Africa and eShandi in Zambia are two standout examples of artificial intelligence and machine learning transforming lending in Africa. These experiences should inspire Cameroon.

Cash-Flow-Based Lending Models and Crowdfunding Platforms: These are financing approaches where lenders assess a borrower’s ability to repay a loan based on future cash flows, rather than relying heavily on collateral or historical credit scores (Kumar et al., 2024; Shneor, 2020). Field research shows that crowdfunding is enabling SMEs in Cameroon to mobilize funding. For example, Tagus Drone created its own platform and achieved a 4400% increase in revenue, while Kiro’o Games used equity crowdfunding to attract strategic investors and slowly build financial stability despite initial cultural and logistical barriers.

Micro-Lending and Flexible Terms: Fintech platforms can profitably offer smaller loan amounts with flexible repayment terms aligned to business cash flow cycles, serving market segments that traditional banks find economically unviable. For instance, MoMoKash in Cameroon offers microloans up to 100,000 CFA Francs to MTN Mobile Money users, with a competitive interest rate of about 7% (0% for repayment within three days). This can serve as a cash flow source for small formal and informal businesses.

Geographic Reach and Accessibility: Low-cost mobile-based fintech solutions overcome geographic barriers by providing 24/7 access to financial services without requiring physical branch visits or extensive paperwork (Epo et al., 2025). That is the reason why mobile money services are spreading rapidly in Africa, despite a relatively low financial development.

In addition to the above advantages, fintech solutions for SME financing create extensive positive spillovers by drastically improving operational efficiency through faster loan processing, enhancing financial inclusion for underserved groups like women and rural entrepreneurs, stimulating competition and innovation within the broader financial sector, and generating valuable economic data that informs better policymaking and support strategies.

Challenges and Risks

Despite significant potential, fintech solutions for SME financing present legitimate challenges requiring policy attention (Agarwal & Chua, 2020; OECD, 2024):

Data Privacy and Security: Alternative data credit scoring involves collecting and analyzing vast amounts of personal and business information, raising concerns about data protection, consent, and potential misuse of sensitive information.

Digital Literacy Barriers: Many SME owners lack the digital skills necessary to effectively navigate fintech platforms, potentially excluding those who could benefit most from improved financial access.

Regulatory Uncertainty: The absence of clear regulatory frameworks creates uncertainty for fintech innovators and consumers alike, potentially stifling innovation while leaving consumers vulnerable to predatory practices.

Algorithmic Bias and Discrimination: Automated credit scoring systems may embed historical biases or create new forms of discrimination, particularly affecting marginalized communities who already face financial exclusion.

Over-Indebtedness Risks: The ease of accessing multiple fintech loans could lead to over-borrowing by SMEs, creating unsustainable debt burdens that ultimately harm business viability.

Policy Recommendations

To harness fintech’s transformative potential for SME financing while proactively mitigating the associated risks, policymakers must move beyond passive observation to active, strategic ecosystem building. Focusing on the context of Cameroon, the following recommendations provide a structured framework for action:

1. Establish a National Fintech Sandbox with a Clear Path to Scale

Action: The Ministry of Finance, in collaboration with the banking regulator (COBAC) and the telecommunications regulator (ART), should immediately launch a controlled regulatory sandbox.

Depth: This is not merely a testing environment. It must be designed as a learning platform for regulators and a bridge to formalization for innovators. Participants should receive tailored guidance, and successful experiments should have a predefined pathway to graduate into fully licensed financial products. The sandbox should initially prioritize testing alternative credit scoring models, crowdfunding platforms, and invoice financing solutions tailored to Cameroonian SMEs.

2. Enact a Robust Data Governance and Consumer Protection Framework

Action: Develop and legislate a modern data protection law that specifically addresses the nuances of financial data used for credit assessment.

Depth: The framework must go beyond general principles. It should mandate algorithmic transparency, requiring lenders to explain in simple terms the key factors behind a credit decision. It must enforce explicit, informed consent for data sharing and establish clear rights for individuals to access, correct, and dispute decisions based on their data. This builds the trust necessary for the ecosystem to thrive.

3. Launch a National Digital Financial Literacy Initiative for SMEs

Action: Integrate digital finance modules into existing SME support programs run by the Ministry of Small and Medium-Sized Enterprises, Social Economy, and Handicrafts.

Depth: Move beyond basic awareness to practical skills. Training should focus on evaluating digital loan terms (APR, hidden fees), understanding data privacy rights, and managing digital financial records to build a positive credit footprint. This empowers SMEs to be informed consumers of fintech products and protects them from over-indebtedness.

4. Foster Open Banking Through Standards and Incentives

Action: Task the banking regulator with developing a phased roadmap for implementing secure Open Banking standards (APIs).

Depth: The goal is to break down data silos. Policy should initially incentivize voluntary data sharing between banks and licensed fintechs, demonstrating mutual benefit. This can evolve into a regulated framework where, with customer consent, SMEs can securely share their transactional data from their bank account to access better loan terms from fintech lenders and vice versa, creating a more competitive and data-rich lending environment.

5. Create a Public-Private Data Utility for Alternative Credit Scoring

Action: Explore the feasibility of a centralized, non-profit credit bureau that aggregates consented data from diverse sources (telcos, utility companies, mobile money platforms, e-government services).

Depth: This addresses the core problem of systemic information asymmetry. By creating a shared infrastructure that generates a more holistic view of creditworthiness, it reduces due diligence costs for all lenders (both fintech and traditional banks) and expands the pool of “bankable” SMEs. The government’s role is to convene stakeholders and ensure governance that balances innovation with privacy.

Implementation Priority: These recommendations are interdependent. The immediate focus should be on establishing the Regulatory Sandbox (1) and the Data Governance Framework (2), as these create the safe space and the essential rules of the game. Concurrently, work can begin on the literacy initiatives (3) and Open Banking roadmap (4), while the data utility (5) is developed as a medium-term strategic project. This coordinated approach positions the government not as a passive regulator, but as an active architect of a more inclusive, efficient, and competitive financial market.

Conclusion

Fintech represents more than a technological advancement for Africa in general and for Cameroon in particular. It constitutes a fundamental tool for unlocking SME potential, addressing the paradox of billions in bank reserves while SMEs remain underfinanced. With 12 million mobile money users already demonstrating digital finance adoption and Camtel’s planned market entry promising increased competition, Cameroon is positioned to bridge its SME financing gap through coordinated policy action. The opportunity to transform the current situation, where SMEs represent only 16.21% of lending portfolios despite constituting 90% of businesses, requires immediate action that embraces innovation while protecting consumers and maintaining financial stability within the CEMAC framework. Cameroon’s policymakers must act decisively to position the country at the forefront of Central Africa’s fintech transformation.

References

Agarwal, S., & Chua, Y. H. (2020). FinTech and household finance: A review of the empirical literature. China Finance Review International, 10(4), 361–376. https://doi.org/10.1108/CFRI-03-2020-0024

Benlamine, P. M., & Tressel, T. (2021). Fintech and financial inclusion in Cameroon. INTERNATIONAL MONETARY FUND.

Bin, J. M., Diangha, S. N., & Ofeh, M. A. (2021). Impact of Access to Credit on the Sustainability of Small and Medium-Sized Enterprises in Cameroon. American Journal of Industrial and Business Management, 11(6), 705–718. https://doi.org/10.4236/ajibm.2021.116046

Björkegren, D., & Grissen, D. (2018). The Potential of Digital Credit to Bank the Poor. AEA Papers and Proceedings, 108, 68–71. https://doi.org/10.1257/pandp.20181032

Epo, B. N., Mougnol, à E. H. W., & Kamdem, Y. A. (2025). Mobile banking and financial inclusion in sub-Saharan Africa: Cost versus geographical constraints. In L’économie au service du bien-être: Mélanges scientifiques en l’honneur du Professeur Fondo Sikod. Afrédit. https://www.researchgate.net/publication/365668994_Mobile_banking_and_financial_inclusion_in_sub-Saharan_Africa_Cost_versus_geographical_constraints

Fedder, M. (2024). Fintech for SME Lending in Africa. MFW4A – Making Finance Work for Africa. https://www.mfw4a.org/blog/fintech-sme-lending-africa

Kenmegni, N. G. R. (2022). Firms’ Characteristics and Cameroonian Small and Medium-sized Enterprises’ Access to Bank Loan. IOSR Journal of Economics and Finance, 13(4), 1–8.

Klapper, L., Ansar, S., & Hess, J., & Singer, D. (2019). Sub-Saharan Africa series: Mobile money and digital financial inclusion. Washington: World Bank.

Kouam, H., & Kouam, S. (2024). Unlocking Access to Finance for Women in Cameroon. Cameroon Economic Policy Institute (CEPI). https://camepi.org/business/unlocking-access-to-finance-for-women-in-cameroon-2/

Kumar, N., Kaveri, V. S., & Shah, N. (2024). Digital Cash Flow Lending to MSMEs: Concepts and Models. NIBM Working Paper Series WP 45/May. https://www.nibmindia.org/static/working_paper/NIBM_WP45_NKVSNS.pdf

OECD. (2024). FinTech lending in Sub-Saharan Africa: Lessons from African economies. OECD.

Rafiq, R. (2021). Can FinTech meet the financing needs of African SMEs? NTU-SBF Centre for African Studies (CAS). https://www.ntu.edu.sg/cas/news-events/news/details/can-fintech-meet-the-financing-needs-of-african-smes

Shneor, R. (2020). Crowdfunding Models, Strategies, and Choices Between Them. In R. Shneor, L. Zhao, & B.-T. Flåten (Eds.), Advances in Crowdfunding (pp. 21–42). Springer International Publishing. https://doi.org/10.1007/978-3-030-46309-0_2

Tantri, P. (2021). Fintech for the Poor: Financial Intermediation Without Discrimination. Review of Finance, 25(2), 561–593. https://doi.org/10.1093/rof/rfaa039

AUTHORS

Yvan Audrey KAMDEM, Research Fellow

Henri KOUAM, Founder and Executive Director