Decentralizing the Cameroonian Economy for Balanced Growth

December 15, 2025

A Review of the Global Environment Facility (GEF) in Cameroon

December 17, 2025

Introduction

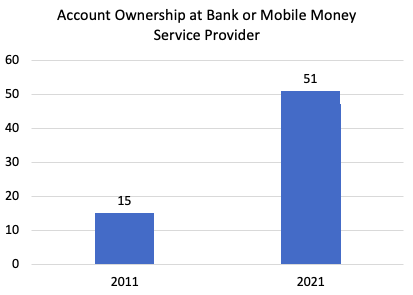

Cameroon has leapfrogged. More adults have access to Mobile Money technologies that allow them to save, transfer, pay, and lend at varying intensities. Is Cameroon a miracle of financial inclusion? Statistics paint a bleak picture, with less than 15% of adults owning bank accounts, but it is usually asserted that over 45% of adults have access to financial services. However, it is misleading to describe Mobile Money access as true financial inclusion. The reason is simple: mobile money has not replaced traditional banking, and entrepreneurs cite a lack of credit as a major challenge to their development. Even if financial institutions chose to leverage mobile money data to improve lending decisions, it is unlikely to yield significant results today.

Source: World Bank

High Bank Account Concentration Does not Translate to Access

Despite the high concentration of banks and MFIs, bank account ownership is low, with only about 12.2% of adults in Cameroon having accounts, compared to a 29% average in Sub-Saharan Africa. Across CEMAC, the financial inclusion rate was around 32% in 2021, with a target to reach 60% by 2027 and 75% by 2030 through regional initiatives. Too few adults own accounts in formal banking institutions, preventing them from developing a credit history and building a financial profile that can make them eligible for loans over the medium term.

In practical terms, this means an agro-manufacturer is unlikely to scale their activities or choose to enter new markets across Africa, as they do not have the financial backing. We dare say that the slow pace of bank account adoption is caused by push and pull factors.

50% of Bank Lending is Directed Towards Large Companies

Commercial bank loans are heavily skewed towards large companies. Data from the Bank of Central States (BEAC) – the Central Bank- finds that large companies received 63% and 60% of total loans versus 17.2% and 21.7% for SMEs in 2021[2] and 2022[3], respectively. Less than 20% of the adult population possesses a bank account (See Figure 2), limiting access to formal bank credit. Even where they have bank accounts, they lack sufficiently acceptable collateral to access credit.

After the COVID-19 pandemic, the share of SME loans in the CEMAC region rose from 15.5% in H2 2021 to 21.7% in Q1 2022, before falling back to 21.3% in Cameroon by Q3

2024[4]. In Cameroon, the largest country in the CEMAC region, larger companies receive 3x more credit than SMEs in 2024 (67 vs 21.3% even as SMEs make up 80% of the industrial sector.

Credit Bureaus are ill-equipped to address the highly informal sectors’ credit needs

The main sources of credit information in CEMAC are limited to the BEAC’s central banking risk database[5] (established in the early 1990s and updated periodically by credit institutions) and microfinance institutions’ risk databases, such as the one managed by Cameroon’s National Council of Credit. However, these databases are fragmented and mostly accessible only within individual countries, limiting their effectiveness for comprehensive credit scoring across the region. While credit bureaus have grown in significance, the absence of movable collateral registries in CEMAC hampers the use of movable assets as collateral, a common practice across other emerging markets.

Banking Services are Perceived to be Too Expensive

All commercial banks and Microfinance institutions are required – BY LAW – to provide 21 services. These range from monthly statements to obtaining account attestations. If the financial sector plays its part, more Cameroonians will likely open bank accounts. Banks should provide the mandated free services to ensure more and more Cameroonians can access banking services.

“There is no point forcing banks to provide services if regulators cannot enforce it. This is why fewer regulations and a more competitive banking sector will be the remedies for high banking costs – not government intervention”.

Ultimately, many micro-SMEs, many of whom are informal, need loans to grow and scale but face social and regulatory constraints, a lack of collateral, and the absence of appropriate credit scoring tools to determine the creditworthiness of borrowers.

Banks Innovate, Not Wait for Deregulation

While most bankers complain about burdensome regulation and compliance requirements, they should innovate faster. While a few banks are using AI tools to improve operational banking, there are few, if any, credit scoring models that consider high-frequency data gleaned from mobile money transactions. Banks should prioritize financial inclusion by ensuring that their policies and approaches support the transition of millions of Cameroonians from the informal to the formal sector.

“Banks can leverage AI tools to create credit scoring models that allow individuals without collateral to borrow and invest in their business. The last thing we should promote is a highly financialized system that contributes very little to the economy”.

Ultimately, consumers and entrepreneurs must take some responsibility by opening bank accounts at formal financial institutions and working towards meeting the criteria to obtain a loan. This includes formalizing their business, keeping a record of accounts, paying their taxes, etc. If banks deem that companies are responsible, they are unlikely to refuse them loans. A more forward-looking system that promotes economic freedom should focus on leveraging innovation to ensure that no one – who can borrow – is left behind.

Mobile money is a form of financial inclusion. But true financial inclusion involves more than money transfer through mobile money and microloans. Policy can incentivize financial inclusion, but some personal responsibility is required to ensure that more people open bank accounts. For financial institutions, they must broaden access to financial services and credit by using newer credit scoring models that use other factors to determine credit creditworthiness of borrowers. We strongly and openly advocate for commercial banks to provide some services, such as checking bank balances, withdrawing cash and obtaining bank statements, and proof of account for free

[1] Mamadou Barry and Du Prince Tchakote. “Financial Inclusion in Cameroon.” International Monetary Fund, (May 2018) : 1-12, file:///Users/henrikouam/Downloads/002-article-A005-en%20(2).pdf

[2] CNSC. “Bank loans to SMEs cross the 20% mark in the first quarter of 2022 (Beac).” Cameroon National Shippers Council, 2022 https://www.cncc.cm/en/article/bank-loans-to-smes-cross-the-20-mark-in-the-first-quarter-of-2022-beac-399

[3] Ibid

[4] BEAC. 2022. Bank of Central African States, Cinquante ans au service de l’intégration des peuples de la CEMAC, https://www.beac.int/wp-content/uploads/2023/10/Rapport-annuel-BEAC-2022.pdf

[5] Nico Halle & Co. 2020. Banking in Cameroon (An Overview), https://fr.scribd.com/document/53121542/BANKING-IN-CAMEROON#:~:text=%2D%20COBAC%20(The%20Banking%20Commission%20for%20the%20six%20Central%20African&text=%2D%20NCC:%20The%20National%20Credit%20Council,SUPERVISORY%20AUTHORITIES/CONTROL.

Henri Kouam is the Founder and Executive Director of the Cameroon Economic Policy Institute (CEPI). A former banker with an authorisation to practice banking at the Microfinance level from the Ministry of Finance, Cameroon, and the banking commission, he contributes to questions around development finance and financial inclusion.

Yvan Audrey Kamdem is a Research Fellow at CEPI and works on issues ranging from the finance sector, financial inclusion, and economic development.

{kind=link}

{kind=link}